So why do Ukrainian companies need to start preparing sustainability reports this year?

In 2025, Ukrainian companies, like their European counterparts, will be subject to new sustainability reporting requirements. This is not merely a trend; it is also a necessity to maintain competitiveness in the global market and to demonstrate responsibility to society. A significant step in this direction is compliance with the requirements of Corporate Sustainability Reporting (CSRD), which will be implemented in the EU in 2025. Consequently, it is imperative for Ukrainian companies to initiate preparations for these new requirements well in advance.

In 2025, Ukrainian companies, like their European counterparts, will be subject to new sustainability reporting requirements. This is not merely a trend; it is also a necessity to maintain competitiveness in the global market and to demonstrate responsibility to society. A significant step in this direction is compliance with the requirements of Corporate Sustainability Reporting (CSRD), which will be implemented in the EU in 2025. Consequently, it is imperative for Ukrainian companies to initiate preparations for these new requirements well in advance.

What is CSRD and why does it matter?

The CSRD (Corporate Sustainability Reporting Directive) is a new European Union directive that requires companies to ensure full transparency in environmental and social responsibility, as well as corporate governance — ESG (Environmental, Social and Governance). According to the latest legislative changes, the CSRD will be implemented in 2025 for many businesses in Europe, and, starting in 2026, will apply to most small and medium-sized enterprises, as well as to non-complex credit institutions.

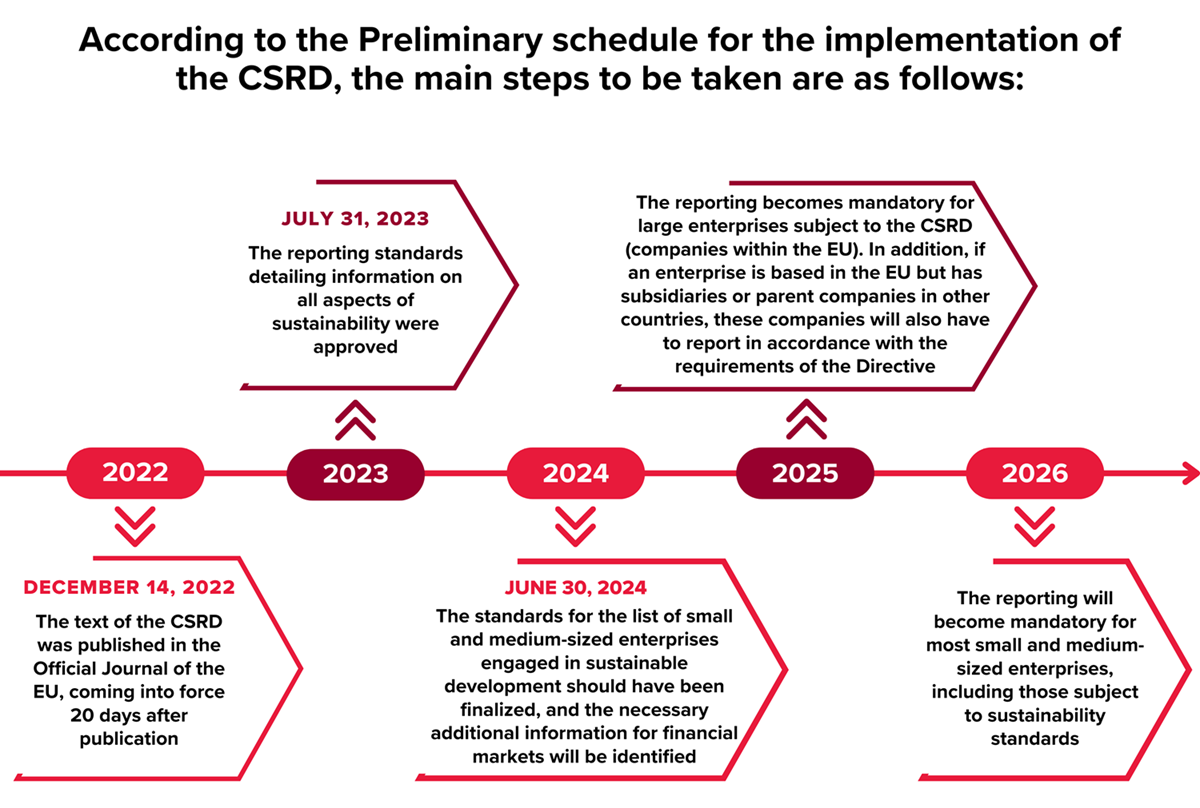

Who is required to report under the CSRD Directive?

- Starting in 2025, large enterprises meeting the CSRD criteria

- Starting in 2026, small and medium-sized enterprises (SMEs) and non-complex credit institutions

- Ukrainian companies operating in the EU or part of European holdings

Companies that export to the EU, have subsidiaries or partners in Europe, must comply with mandatory reporting requirements.

The significance of timely preparation for reporting

For Ukrainian companies that aim to operate in the European Union or conduct business with European partners, the compliance with CSRD standards becomes not only a crucial factor for building a positive image and sustainability in the face of global economic changes, but is also a requirement of European regulators.

Key benefits of preparing sustainability reports:

1. Enhancing corporate reputationCompliance with the CSRD requirements will demonstrate the company’s commitment to adhering to European and international standards, which will strengthen the company’s reputation among investors, partners and customers.

2. Attracting investment

Investors are paying increasing attention to the sustainable development of companies. Thus, the companies that comply with ESG requirements are better positioned to attract additional funding. Sustainability is an important criterion for raising capital, especially from the international donors and financial institutions.

3. Increasing efficiency and minimizing risks

Preparing for reporting enables companies to better assess environmental and social risks. Timely implementation of the strategies aimed to reduce harmful environmental impacts and improve working conditions is becoming an important part of a sustainable development strategy.

4. Meeting the requirements of international law

The Ukrainian companies with business ties to the EU should be preparing for the transition to new reporting standards. Adherence to the CSRD requirements not only mitigates legal risks but also enables companies to circumvent fines and penalties for non-compliance.

How to prepare for ESG reporting?

Preparing for the implementation of sustainability reporting requires a systematic approach and interaction with all business units. To do this, you will need to:

- Analyze the current sustainability strategy and align it with the standards set by the CSRD.

- Develop internal policies for collecting, processing and reporting information on environmental, social and governance aspects of operations.

- Establish appropriate monitoring and reporting systems that enable timely submission of reports that meet international standards.

- Select and use the necessary software to automate the processes of collecting and calculating the necessary reporting metrics.

What are the requirements for non-European companies?

According to the CSRD, companies from other countries doing business in the EU must consider sustainability requirements in their reporting. This means that:

- Transparency of information: Companies should disclose information on the environmental, social and corporate governance impacts of their operations, including climate change, use of natural resources and treatment of employees and suppliers.

- Integration with the EU taxonomy: Reporting should be consistent with the EU Taxonomy, which defines how a business can be recognized as environmentally sustainable, enabling investors to assess the environmental performance of assets and operations.

- Development and compliance with sustainable development policies: In particular, companies must demonstrate how they manage resources and waste, implement policies to reduce greenhouse gas emissions and ensure a circular economy that includes recycling and reuse of resources.

Ukrainian regulatory framework: What to prepare for

The government’s adoption of the Sustainability Reporting Strategy on October 18, 2024, in accordance with the EU Corporate Sustainability Reporting Directive (CSRD) and European Standards (ESRS), presents new challenges for the Ukrainian business sector. Here’s a look at what awaits Ukrainian businesses can expect over the next three years and what steps they should take to successfully adapt to the new requirements.

What will change in the area of reporting?

The introduction of sustainability reporting envisages the implementation of European standards, which should harmonize the Ukrainian legal framework with EU directives. The government expects that this will create three pillars for future development:

- Achieve transparency in reporting

- Develop a unified platform for submitting non-financial reporting

- Attract foreign investment by increasing the level of investor confidence.

According to the Strategy, the changes are already underway and will be addressed in three dimensions simultaneously. The primary challenge will be to align Ukrainian legislation with European standards. The key dates are as follows:

- By November 2024, the translation of Directive (EU) 2022/2464 should have been completed.

- Starting from December 2024, the tables of compliance with Ukrainian legislation are already being prepared.

- In March 2025, a draft law amending the Law of Ukraine “On Accounting” is expected to be submitted.

By the end of 2025, the unified electronic reporting format is scheduled to be developed. Specifically, the unified reporting rules are to be finalized by December 2025, and the unified reporting platform is to be developed and approved by March 2026. The specific design and functionality of the platform are yet to be determined. However, at the time of its approval and testing, Ukrainian companies should take the necessary measures to collect information for reporting, analyze it, and set goals for future years.

The final and most significant challenge for entrepreneurs will be the format of sustainability reporting as part of a company’s non-financial reporting. At this time, the Strategy offers no clear guidance on the form of reporting, as it only states that an official translation of ESRS standards will be available for Ukrainian companies in the summer of 2025. However, the Strategy does not offer any guidance on how to adhere to these standards or prepare the necessary reports.

Conclusions

Sustainability reporting is an integral component of modern business practice. The companies that neglect to initiate preparations for this reporting may find themselves at a competitive disadvantage. Ukrainian companies must adapt to the CSRD requirements now, in order to be ready for the changes coming into effect in 2025. This will allow them not only to meet the international requirements but also to ensure stable, efficient and sustainable development in the future..

Companies that fail to adapt to the new standards risk losing competitive advantages and development opportunities in the EU.

Don’t delay preparing — start adapting to CSRD now!